Discover How to Build a Retirement Plan Designed to Last Longer Than You®

...From the Comfort of Your Home

Without the 1% fee. Without the high-pressure sales pitch dressed up as a consultation.

The Retire on Time Planning Kit gives you access to twelve retirement planning tools (the same ones Michael Decker, NSSA® uses with his clients) so you can explore your options and pick the right path for you, on your own terms, for $97.

Instant Digital Access · Free U.S. Shipping · 30-Day Money-Back Guarantee

What the Retire on Time Home Planning Kit Is

Most retirement advice falls into two categories.

It's either too generic to be useful (pamphlets, blog posts, the default "60/40 portfolio and stay the course" framework you've heard your whole working life).

Or it's behind a "trust me" wall. Many advisors won't tell you what they're actually going to do until after you've become a client. The process, the strategies, the specific moves... All of it gets explained on the other side of your signature, not before. Imagine buying a car that way. Or a house. Or anything else that mattered.

The Retire on Time Planning Kit is the thing in between.

It's a complete set of working materials you can use to build your own retirement plan. The goal is to let you explore your options without bias or sales pressure. It's designed for people who want to retire within five to 10 years (or are already retired) and want to actually understand how it all works.

Here's Everything Inside Your Retire on Time Planning Kit

The How to Retire on Time Book

The full framework in book form. Read it in a weekend or listen on a walk. The book lays out the key philosophy, the tax strategy, and more without industry jargon. You'll get a digital copy and a physical copy shipped to you.

Value: $19

The Retire on Time Workbook

This is where reading becomes planning. The workbook walks you through the exact exercises (income strategies, tax-minimization strategies, healthcare planning, and more) that turn the framework into your plan. Designed to be completed at your kitchen table, at your own pace. You'll get a digital copy and a physical copy shipped to you.

Value: $49

The Retire on Time Checklist

A step-by-step checklist on how to put your plan together based on what we believe is the correct retirement planning sequence so that you can explore how to potentially get more out of your money.

Value: $12

The Retire on Time AI Prompt List

A curated set of AI prompts designed specifically for retirement planning so you can ask better questions as you go through the planning process. Use your preferred AI, whether thats ChatGPT, Claude, Grok, Gemini, or something else.

Value: $17

The Retirement Planning Calculator

Use the same planning tool that the author uses with his clients every day. See your starting portfolio, projected income, and plan longevity at a glance. Model different scenarios (IRA to Roth conversions, Stress Tests, etc) so you can see how the decisions you're making today may affect your retirement.

Value: $97

The Social Security Optimizer

The difference between claiming Social Security at 62 and claiming at 70 can be hundreds of thousands of dollars over the life of your plan… And the "right" answer depends on your income needs, your tax bracket, your spouse's benefits, and how long your plan needs to last. This optimizer walks you through the variables, shows you the break-even math, and helps you coordinate your claiming decision with the rest of your retirement income plan so you're not leaving money on the table or claiming too early out of fear.

Value: $47

The Tax Return Simulator

Most retirees never see how one decision (a Roth conversion, a withdrawal from the wrong account, a capital gain at the wrong time) can quietly push them into a higher tax bracket or triggers IRMAA surcharges. This simulator lets you model your return, so you can see the potential tax impact before you make the move. Spot the levers many people miss, coordinate your income and tax strategy, and stop overpaying the IRS in retirement.

Value: $97

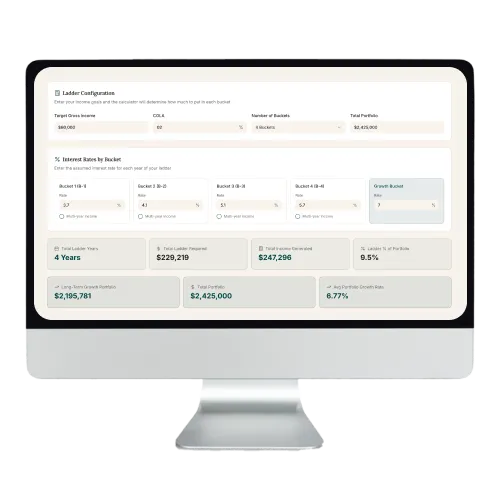

The Bucket (Ladder) Planner

The Bucket Planner helps you map your assets across short-term, mid-term, and long-term buckets so you always know which dollars you'll spend first and which ones have time to grow.

Value: $47

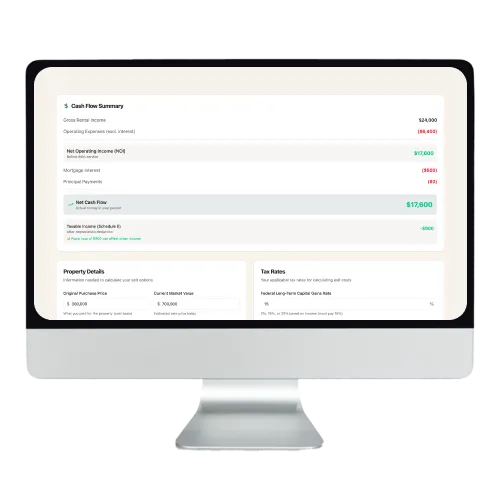

The Real Estate Exit Planner

Run an analysis on your investment real estate as you explore and compare your exit strategies. Discover tax efficient exit strategies that are designed to help you maintain/increase your cash flow while deferring taxes for life.

Value: $97

The Estate Planning Software

Gain access to Wealth.com, a professional estate planning platform that can help you create your living trust, pour-over will (last will and testament), financial power of attorney, and medicare directive, included as a part of the kit at no additional cost.

Value: $599

The How to Retire on Time Audiobook

Listen on walks, in the car, or while you make breakfast. The full book, narrated, so you can absorb the framework however you learn best.

Value: $19

Weekly Live Q&A with the Author

Every week, Michael Decker, NSSA® goes live to share market updates, a few timely retirement planning tips, and answer questions submitted by Kit owners in real time, on camera, with no filter

Value: $197

Everything Above, Together:

The How to Retire on Time Book - $19

The Retire on Time Workbook - $49

The Retire on Time Checklist - $12

The Retire on Time AI Prompt List - $17

The Retirement Planning Calculator - $97

The Social Security Optimizer - $47

The Tax Return Simulator - $97

The Bucket (Ladder) Planner - $47

The Investment Real Estate Exit Planner - $97

The Estate Planning Software - $599

The How to Retire on Time Audiobook - $19

Weekly Live Q&A with the Author - $197

Total Value: $1,297

Today: Just $97

Instant Digital Access · Free U.S. Shipping · 30-Day Money-Back Guarantee

Here's What Makes The Retire on Time Home Kit Different

Most retirement "plans" start with a product. An annuity. A fund. A portfolio allocation someone wants to sell you. We don't believe in that approach… And we don't believe in the premise behind it.

We believe you should put your plan together first (your projections), then explore strategies second to help you get more out of your money, and then determine which investments or products are right for you.

There is no such thing as a perfect investment, product, or strategy. Nothing does everything well. Every investment or product you pick has benefits and detriments associated with it. That's why it's so important to pick your investments and products last. Your portfolio must be aligned with and support your plan and strategies, not the other way around.

That's why the Retire on Time Planning Kit is built on three principles many advisor offices will never tell you out loud:

1. You deserve neutrality, not a sales pitch.

Instead of steering you toward one product, the Kit walks you through your options side-by-side, including the benefits and the detriments of each investment, product, and strategy, so you can make an informed decision about what actually fits your life.

No pressure. No push. No "trust me on this one." Just the information you need before you can make an informed decision based on what is right for you.

2. Tax planning matters and applies to everyone, not just the 'rich.'

Taxes are likely your biggest expense in retirement and an important part of every retirement plan. The problem is too many advisors claim "I can't give tax advice" as they recommend strategies that are tax inefficient.

The Kit includes an entire section dedicated to helping you read your own tax return, spot potential inefficiencies many smart people miss, and coordinate your income and tax strategy with the intention of keeping more of what you've spent a lifetime working for.

3. The key to making your money last is having two portfolios.

Most people have a portfolio built for up markets, not down markets. No one can time the market, which is why we believe it is so important to have two portfolios; one for when markets are up, and a back up for when markets are down.

Just like a city has a reservoir of water in case of a drought, we believe that a retiree should have reserves (investments or products that can't lose money) incase of a market crash.

Why does this matter so much? In retirement, when you take income from an account that is down, you accentuate the losses making it more difficult to recover. You lock in the damage that hurts your ability to stay retired. The book (and kit) show you several ways to solve this issue.

Is the Retire on Time Planning Kit Right for You?

Before you click that button, it's worth making sure this is actually a fit. We'd rather you pass than buy something that isn't right for where you are.

This Kit is for you if...

You're 5 to 10 years from retirement, or already retired, and you want a clear plan instead of a vague hope.

You've sat through advisor meetings and walked out more confused than when you went in.

You want to understand why a retirement strategy works, not just be told to trust it.

You're tired of being sold products and would rather evaluate your options neutrally, with the benefits and the detriments laid out side by side.

You want to coordinate your income plan, your tax plan, your Social Security, and your home equity as one strategy, not four disconnected decisions.

You'd rather explore your options in peace at your kitchen table rather than sit through another sales pitch in an advisor's office.

This Kit is not for you if...

You're looking for a magic formula, a hot stock tip, or a "get rich" shortcut.

You want someone else to make every decision for you without understanding why.

You're not willing to spend a few hours actually working through the exercises (the Kit only works if you do).

If the first list sounds like you, keep reading. If the second list sounds like you, this Kit honestly isn't the right fit… And we'd rather tell you that now than have you buy something that sits on your shelf.

Your 30-Day "Build the Plan First" Guarantee

Here's how confident we are that this Kit will change the way you think about retirement:

Work through the Kit for 30 full days. Complete the workbook. Use the calculators. Review the tax exercises. If you don't feel more informed, more in control, and more clear about your retirement than you did before email us, and we'll refund every penny. No forms. No phone calls. No questions asked.

You either walk away with a plan you built, understand, and own or you walk away with your money back. The only thing you can't walk away from is another year of uncertainty.

Instant Digital Access · Free U.S. Shipping · 30-Day Money-Back Guarantee

About Michael Decker, NSSA®

Michael Decker is the founder of Kedrec Wealth, a Kansas-based Registered Investment Advisor firm, and the author of How to Retire on Time, an Amazon #1 Best Seller that teaches how to build a plan designed to last longer than you®.

But the truth is, the Planning Kit and the book came from years of industry frustration. Early in his career, Michael kept asking questions that others didn’t want to answer or admit to (1% fees, portfolio management strategies, taxes, etc). The answers were almost always the same: "This is the way things are." "This is how it's done." "Don't overthink it."

The more Michael questioned the industry, the more he realized the industry was a bunch of people selling a product while holding a license. "Planning" was really the path that led to selling their product.

He wrote How to Retire on Time as an argument against oversimplified strategies and clichés that may not be as financially prudent as some would suggest. The Planning Kit is the working version of that argument, built to help individuals and couples see how things actually work, not how a salesperson wants them to.

The kit follows the same framework Michael walks his clients through, available for you to complete at your kitchen table, at your own pace.

Frequently Asked Questions

I'm already retired. Is this kit still for me?

Yes. The framework applies whether you're approaching retirement or already in it. If you're retired, the workbook will help you stress-test the plan you have, the calculators will help you see whether your withdrawal strategy is sustainable, and the tax simulator will help you spot opportunities most retirees miss for years. The Kit assumes you're either getting ready or already living it… Both work.

I'm 10+ years from retirement. Is this too early?

No. The earlier you understand the framework, the more decisions you get to make on purpose rather than by default. Roth conversions, asset location, reserve building; these all compound over time. Starting a decade out gives you more levers to pull.

How do I access the kit after I buy?

Immediately. You'll get instant digital access to everything in the Kit (the book, the workbook, all of the calculators, the audiobook, the AI prompt library, and your Wealth.com estate planning account) the moment you check out. Your physical Kit (book, workbook, checklist) ships to your door within a few business days.

Is this going to try to sell me something else?

The Kit is designed to stand on its own, and many readers go through it and run their plans successfully on their own. There's no mandatory upsell sequence and no high-pressure follow-up. If you decide after going through the Kit that you'd like to talk to our team, that option is available, but it's genuinely optional. The Kit is structured to be fully useful whether you ever pursue it or not.

What's included in the $97?

Everything. Instant digital access to all twelve tools, your physical Kit shipped to your door, the audiobook, your Wealth.com estate planning access, and ongoing access to the Tuesday Live Q&A. One payment, no subscription, no upsells required.

Do I need to be good with spreadsheets or technology to use the calculators?

No. The calculators are built to be usable by anyone comfortable with basic financial concepts.

Is this investment advice?

No. The Kit is educational. It's a set of tools, frameworks, and working materials, not personalized advice for your specific situation. Personalized advice requires an advisory engagement with written terms.

What if I don't think the kit is worth it?

If you go through the Kit within 30 days and decide it isn't what you hoped, email us, and we'll refund the full $97. Keep the materials. No forms, no calls, no questions.

Still have a question we didn't answer? Email [email protected] and we'll get back to you within one business day, before or after you purchase.

Ready to Get Started?

Everything in the Planning Kit, available the moment you check out. Physical Kit ships within 2 business days.

Instant Digital Access · Free U.S. Shipping · 30-Day Money-Back Guarantee

Terms and Conditions Privacy Policy

Copyright © 2026• Kedrec LLC • All Rights Reserved

This site is not a part of the Facebook website or Facebook Inc. Additionally, This site is NOT endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.

This content on this website is provided for informational purposes only and is not intended to serve as the basis for financial decisions. It should not be construed as investment advice or a recommendation.

Investment advisory services are offered through Kedrec, LLC, a Kansas state Registered Investment Advisor. Insurance products and services are offered through its affiliate, Kedrec Legacy, LLC. We are not affiliated with the US government or any governmental agency.

Investing involves risk, including possible loss of principal. No investment strategy can guarantee success, ensure a profit or guarantee against losses. Insurance product guarantees are backed solely by the financial strength and claims-paying ability of the issuing company.

Insurance and annuity products involve fees and charges, including potential surrender penalties. Annuity withdrawals are subject to ordinary income taxes and potentially a 10% federal penalty before age 59-1/2. Life insurance generally requires medical and potentially financial underwriting to qualify for coverage. Optional features and riders may entail additional annual cost. Product and feature availability may vary by state.

Tax, legal and estate planning services are available only to planning and/or wealth management clients. Tax, legal and estate services provided by our network of tax and legal professionals. Always consult with qualified tax/legal advisors regarding your unique circumstances.